Demystifying Revenue Structures for Battery Energy Storage Systems (BESS)

For developers and investors of Battery Energy Storage Systems (BESS), securing predictable revenue streams is increasingly crucial for project bankability. Tolling agreements, a concept long-established in other industries and asset classes, and now gaining significant traction in the energy storage sector, are a proven tool do de-risk volatile merchant revenues. In this post, we'll break down what a BESS tolling agreement is, how it differs from other revenue models and how our proprietary platform LAYR enabled us to secure two innovative multi-asset capacity tolls with Vattenfall and RWE.

Revenue Stream: Fully Merchant

Mode: The asset receives the market price based on the performance of the trader.

Main benefits: Higher returns can be achieved during favourable market conditions.

Main Risks: Market risk - returns can be less favourable than expected or diminish over time. Performance risk - optimizer can underperform.

Revenue Stream: Fully Tolled

Mode: The asset receives a fixed income and has no exposure to market volatility.

Main benefits: The asset receives a fixed income and has no exposure to market volatility. Stable, planable, secured cash flow that enables project finance.

Main Risks: Counterparty (credit) risk, opportunity losses in favourable market conditions, contractual obligations in tolling contract.

Revenue Stream: Hybrid

Mode: A % share of the asset is tolled, the remaining asset receives the market price.

Main benefits: A stable cash flow that allows a higher loan-to-cost ratio while keeping some of the upside for higher equity returns in favourable market conditions.

Main Risks: Substantially the same risks as for fully merchant and fully tolled, but to a lesser degree.

Revenue Stream: Floor

Mode: The asset receives the market price with a discount in exchange for a minimum payment in case the market price drops below the floor.

Main benefits: Downside protection for market periods with low returns, participation in high market prices (albeit with a discount), might enable project finance (if the floor level is high enough).

Main Risks: Sacrificing upside in return for a the downside hedge, counterparty (credit) risk, Performance risk: trader can underperform, Market risk: only extreme downside is protected.

The Challenge of Pure Merchant Revenue

For lenders, financing BESS assets can be challenging compared to other asset classes, due to the volatile nature of the expected returns, i.e. the market risk associated with BESS revenues. While a few banks are comfortable financing smaller BESS assets with fully merchant revenues, the depth of the financing market for assets exposed to merchant risk is limited, as is the typically achievable loan-to-cost ratio. We've observed that many banks are now hesitant to finance BESS assets without at least 50% of their revenues secured through a bankable tolling agreement, or charge high interest premiums or offer very low loan-to-cost ratios. Therefore, securing cash flows through a tool such as tolling becomes increasingly relevant given increasing project- and portfolio sizes and corresponding capital needs.

Why is this the case?

- Market Volatility: Electricity markets are highly volatile. While BESS assets are uniquely positioned to profit from this volatility, it's impossible to predict with certainty what market conditions, and therefore BESS revenues, will look like in the long term over the asset life time. This uncertainty makes it difficult for lenders to project future cash flows.

- Performance Risk: BESS assets are an active asset class, meaning their revenues depend on skilled commercial management. A poor operational strategy can lead to underperformance. For a lender, this introduces significant risk, as the project’s ability to service its debt relies directly on the performance of the Optimizer.

- Nascent Asset Class: Compared to mature asset classes like real estate, BESS is still a relatively new asset in the German and European markets. The limited availability of historical data and long-term performance track records makes lenders and investors naturally cautious.

Lenders are primarily concerned with getting their principal and interest back. Predictable, long-term cash flows increase their trust in the project's ability to cover the debt service for the loan's tenure. This is where a tolling agreement becomes essential for bankability.

What is a Tolling Agreement and how does it help?

A tolling agreement for a BESS asset is a fixed-price capacity off-take agreement, in other words, a battery "lease". In this arrangement, the asset owner makes all or a portion of the battery's capacity exclusively available to a third-party off-taker in exchange for a regular, fixed payment. This provides a stable, predictable revenue stream for the BESS owner, while giving the off-taker access to battery capacity without having to build and operate it themselves. The off-taker effectively takes a long-position in the market, while the asset owner transfers the primary market risks (revenue volatility) and trading performance risks to the off-taker, at the cost of losing out on higher-than-expected revenues. This leaves the asset owner primarily responsible for managing the asset performance and availability. The asset owner's exposure is therefore mainly limited to asset-related risks, such as project delays, maintenance, downtime, and battery performance.

The steady cashflow secured through the toll effectively reduces the risk for the asset owner and lender, making BESS projects more bankable.

💡 Bankability and a strong Counterparty

For a BESS project to be bankable, the cash flows must be secured by a strong counterparty. In a BESS tolling agreement, the counterparty is the off-taker who pays for the battery's capacity.

A bankable counterparty is a financially stable and creditworthy entity, such as a investment-grade utility or other company, with a robust balance sheet and a high credit rating. Lenders scrutinize the credit risk of the off-taker, to ensure it can fulfil its long-term payment obligations.

💡 Types and Terms of Tolling Agreements

The need and basic concept of tolling agreements are clear, but not every toll is the same. So, next we are going to take a look at the different types we observe in the market. The two most prominent forms are:

- Physical Tolls: The off-taker is interested in the physical battery; and doesn't just lease the "capacity", but the entire physical battery, onboards it to its balancing group and asset fleet, and commercializes it in its preferred way.

- Financial Tolls: The off-taker takes market exposure by guaranteeing a fixed price against a floating index (like e.g. the day ahead market), settling the trade financially. The asset is often physically onboarded and traded on the wholesale markets via a third party.

The majority of tolls discussed in the market range between 5 and 7 years (up to 10 years) with prices typically centered around 110k€ and 150k€ per MW per year, depending on the start date, asset parameters, tenure, off-taker appetite and contractual terms.

💡 Typical Off-Takers include

🔌 Utilities

🛢️ Oil & Gas Majors

🏦 Financial Players

📈 Trading Houses

Why aren't there more BESS Tolling Agreements in the Market?

By now the relevance and positive impact of tolling agreements on BESS projects are clear. Nevertheless, according to Aurora, there have only been 6 tolling agreements in Germany, half of which have been signed by terralayr.

💡 To close these agreements terralayr and our contract partners had to overcome many of the complexities typically associated with BESS tolling contracts:

- Bespoke Nature: Tolling agreements are typically bespoke, long-term contracts (often 5+ years). Without a "market standard," tenders can become overly complex, and negotiations can drag on. Offers often come in different formats, making them difficult to compare.

- Long-Term Risk Mitigation: The long duration of these contracts means they must account for numerous "known unknowns," and "unknown unknowns," and fairly distribute them between the asset owner and the toller. This can lead to lengthy discussions on clauses related to things like Redispatch or "Change-in-Law."

- Project Finance Requirements: Since tolling agreements are often used to secure project financing, the requirements of lenders must be incorporated into the contract. This adds another layer of complexity on top of the needs of the asset owner and the toller.

- Commercial Gap: Asset owners often benchmark against merchant revenue predictions or historical performance, while tolling prices must account for uncertainty and long-term risk. This often leads to a commercial gap that needs to be overcome during negotiations.

The Future of BESS Tolling: A strategic hybrid Approach

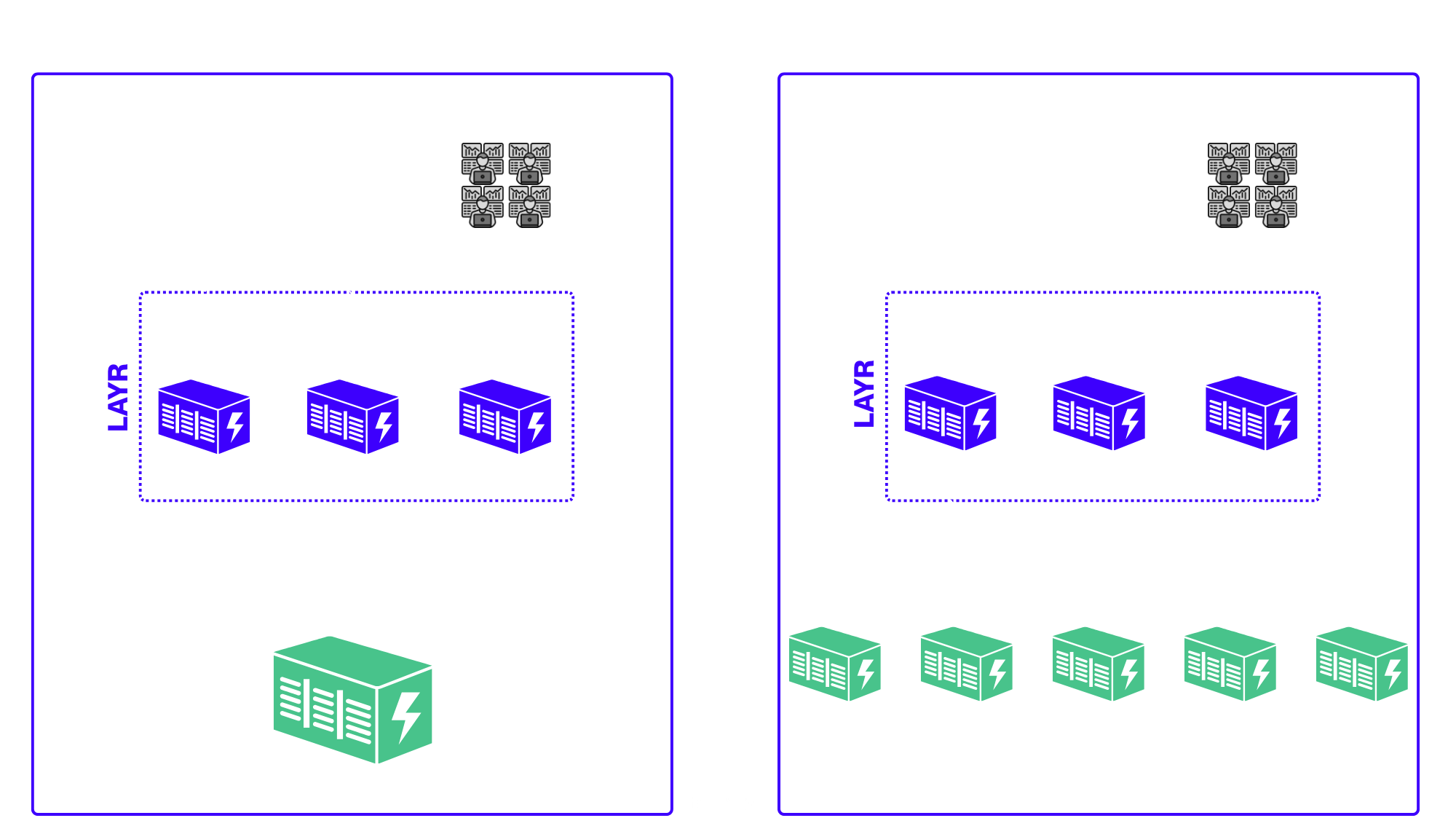

As the energy storage market matures we expect to see the continued evolution of innovative tolling structures. At terralayr, we're at the forefront of this trend. We initially sought a solution for our own asset fleet and have since further developed our proprietary platform LAYR to overcome market challenges present for all project developers. At the core is our belief that via asset aggregation of medium sized assets origination on portfolio level becomes available while asset disaggregation enables custom off-take structure structures, which can be changed throughout an asset's lifetime.

1. Diversification of revenue streams: flexible slicing of a physical asset into tolling and merchant slices throughout asset lifetime, without physical restrictions or additional hardware required, enabling custom off take structures.

2. De-Risking merchant: no lock-in with a single optimizer and diversification via pool of top-tier-optimizers already onboarded to LAYR between which we can flexible allocate capacity.

3. Reduction of overhead and time-to-market: access to our robust and scalable off-taker framework agreements enabling fast, repeatable off-take for project developers and asset owners.

Summary: The terralayr Advantage

While a fully merchant revenue structure seems obvious at first sight, the triple risks of market volatility, operational risk, and the asset class's nascent status demands a de-risked approach to achieve bankability.

The tolling agreement emerges as the critical solution: a fixed-price capacity off-take that acts as a battery lease. By transferring primary market risk to a creditworthy counterparty (the off-taker), the asset owner secures the stable, predictable cash flow required by lenders.

While various forms of tolling exist, we believe the path forward is a strategic hybrid approach. This is why we developed our platform LAYR, allowing us to virtually split BESS capacity. This flexibility allows asset owners to customize their risk-return profile, securing the essential guaranteed revenue through tolling while retaining a merchant share to capture upside potential. We believe the combination of physical assets, software and innovative commercial models is key to accelerate BESS deployment and drive the creation of a more resilient grid.

Additional Material from terralayr

-

Join our CCO Mikko Preuß in Aurora Energy Research latest webinar on the role of tolling agreements in Germany’s future BESS market.

Go to Webinar! -

Sign up to our newsletter to not miss any upcoming webinars or other exciting news from terralayr!

Sign up to our Newsletter!